19 May 2026

Mapping the Journey of Funds: From User Onboarding to Ongoing Assistance in Portable Payment Solutions

Portable payment solutions have transformed how individuals and businesses handle money transfers, yet the underlying path that funds take from the moment a user signs up remains less visible to most observers. Researchers at institutions like the Bank for International Settlements have documented steady growth in these systems, with transaction volumes rising across regions as digital wallets integrate with everyday commerce. This journey begins with onboarding and extends through continuous support structures that keep accounts functional and secure.

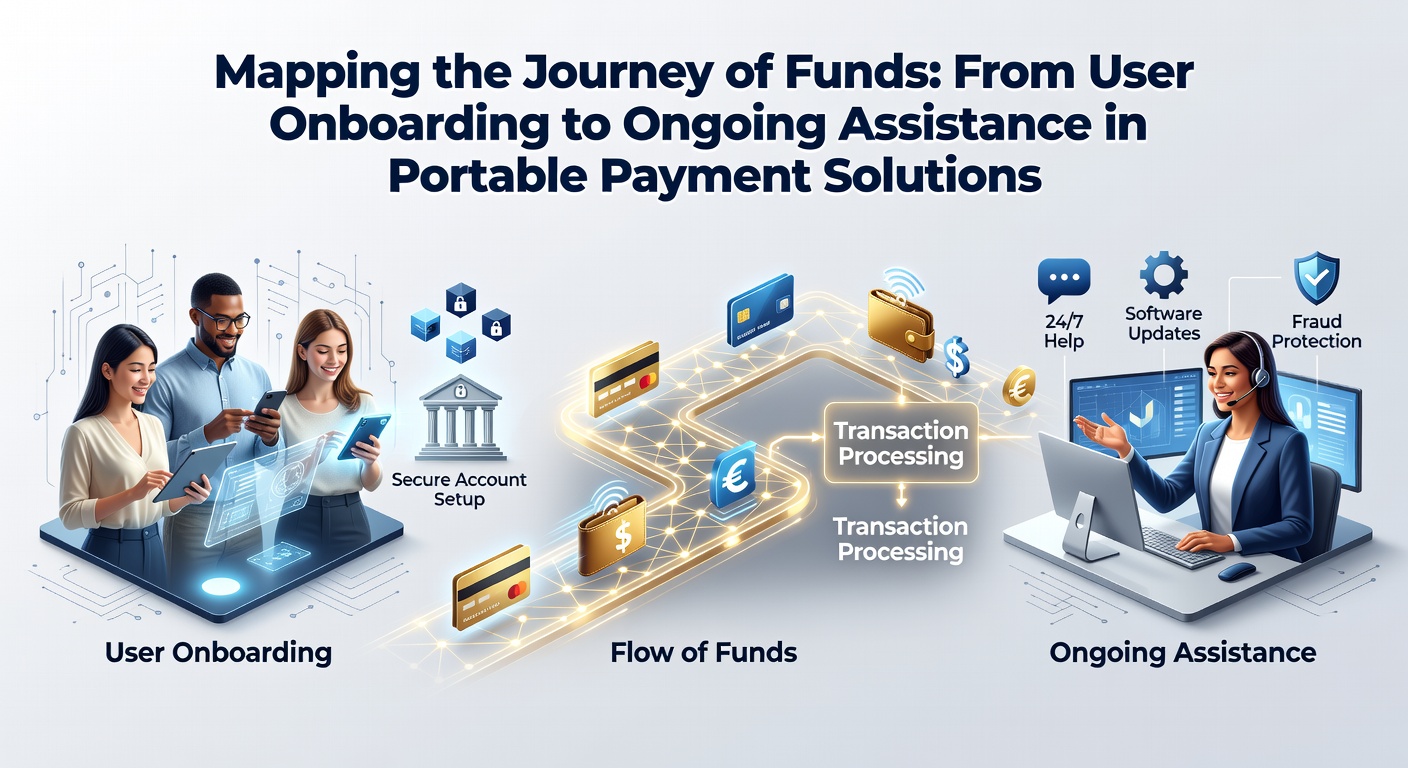

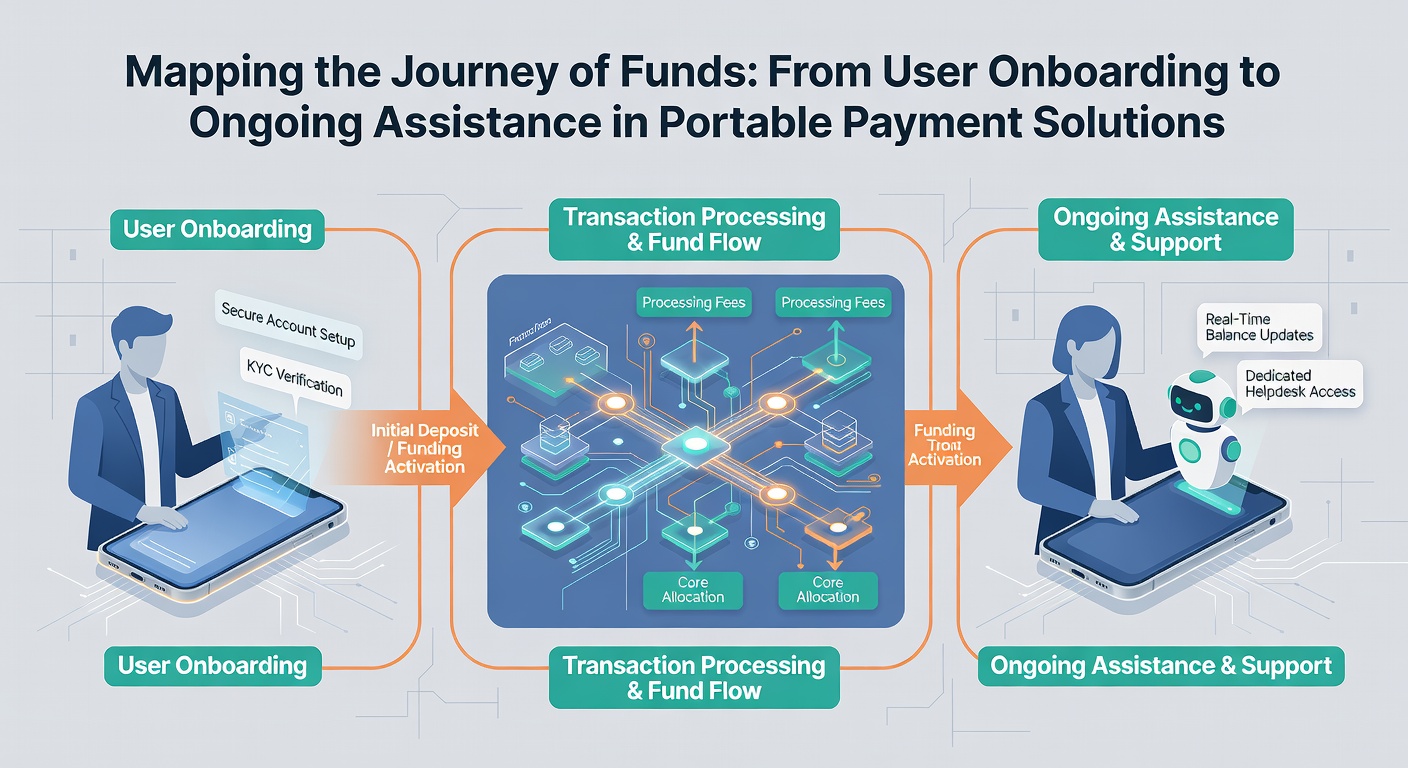

Initial Onboarding and Account Setup

Users typically start the process by downloading an app or accessing a web portal, where basic details such as name, address, and identification documents get submitted for verification. Automated systems cross-check information against government databases in real time, which speeds up approval while reducing manual reviews. Once verified, the account activates and links to external funding sources like bank accounts or cards, creating the first conduit for money movement. Observers note that this phase often takes only minutes in well-designed platforms, though regional regulations can extend timelines when additional checks apply.

Fund Integration and First Transfers

After activation, funds enter the ecosystem through deposits or transfers that settle according to network rules. Portable solutions frequently employ instant or near-instant rails for these movements, allowing balances to update immediately while backend settlement occurs later. Data from central banks shows that such mechanisms have lowered friction in cross-border and domestic payments alike. The system then maintains ledgers that record every incoming amount, ensuring traceability from source to destination without exposing full user histories to third parties.

Transaction Routing and Security Layers

Once funds sit in an active wallet, each transaction follows predefined routes that balance speed with compliance requirements. Encryption protocols protect details during transmission, while fraud-detection algorithms scan patterns for anomalies before authorization completes. Those who have studied these flows point out that portable payment platforms often partner with established card networks or banking partners to clear payments efficiently. In May 2026, several providers updated their routing logic to incorporate newer instant-payment standards rolled out by the European Central Bank, which further shortened settlement windows for participating users.

Balance updates appear in user interfaces almost instantly, yet the actual movement of value continues through clearing houses or interbank systems operating in the background. This separation between visible activity and underlying settlement helps maintain liquidity while users experience seamless interactions.

Ongoing Assistance and Account Maintenance

Support does not end after the first transaction. Automated tools monitor accounts for unusual activity and trigger alerts or temporary holds when needed. Human support teams step in for complex cases such as disputed charges or failed transfers, drawing on detailed transaction histories to resolve issues. Industry reports indicate that many platforms now integrate chat-based or in-app assistance that routes queries directly to specialists familiar with specific payment corridors. These layers of help keep funds accessible and accounts operational over months or years of regular use.

Regulatory Oversight and System Updates

Government agencies track portable payment ecosystems closely, requiring regular audits and compliance reports. The Reserve Bank of Australia, for example, has published guidelines on consumer protection that influence how providers handle fund recovery after unauthorized access. Updates to these frameworks often prompt platforms to adjust onboarding questionnaires or enhance encryption standards. Observers tracking developments note that such changes tend to roll out in phases, giving users time to adapt without service interruptions.

Conclusion

The complete path of funds in portable payment solutions stretches from the first verification step through every subsequent transfer and support interaction. Central banks and research organizations continue to gather data on these flows, revealing patterns that help refine both technology and policy. As systems evolve, the emphasis remains on maintaining clear records, swift assistance, and reliable movement of value across digital channels.